Thirty Trillion Dollars! That staggering amount is what studies predict will be transferring from Baby Boomers to their heirs in the coming years (i). Yet nearly 70 percent of family wealth transference and business succession plans fail, with the vast majority (actually 60 percent) of failures attributable to poor family communication and heir preparation (ii). This begs the question “How can Baby Boomer’s parents better prepare their heirs to be successful stewards of the savings that they have spent their lifetimes accumulating?

Tackling this daunting challenge may best be done by first having an objective appreciation of our heir’s cultural differences, then identifying what skills they need to succeed, followed by an objective diagnosis of where they may fall short. Then we can more effectively provide them guidance and with the resources they may need.

The reality is, Baby Boomers have accumulated a level of assets that is significantly greater than that of their parents, and will likely far exceed what the next generation may be able to accumulate. Boomer’s good fortune stems from an extended period of economic growth and stability occurring during their peak earning years (their aggregate net worth has quadrupled since the last 1980’s). This combined with the considerable appreciation of non-financial assets such as real estate (iii), has provided a near perfect good storm. When contrasted to the challenges many Gen Xers (born 1965-85) and Millennials (1985-2004) have experienced, especially since the Great Recession of 08-09, the resulting asset gap becomes more understandable.

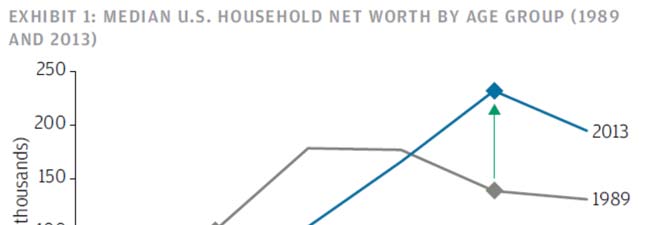

As the graph below shows, the median household net worth for today’s 35 to 44 year olds is approximately $47,000, compared with $102,000 for those of a similar age in 1989 (adjusted for inflation). No small wonder it has been said that this younger generation may be the first in our country’s history to hold a more pessimistic view of their future opportunities compared to their predecessors. Combine that with the entitlement that many exude, it’s not surprising that cultural perspectives may vary.

A young person’s ability to successfully launch themselves in several crucial life areas has traditionally served as a competency gauge, giving the impression of becoming one’s “own person,” grown-up and responsible. Knowing the functional and cultural differences between generations can provide valuable insight:

1. Career Success: Boomers value hard work almost to an extreme. Common with this “live to work” philosophy were 50 to 60 work weeks and a consequence that family and health, at times, ranked a distant second. They found an abundance of opportunity, with consistent reward and advancement for their hard work ethic. This fostered a perception that floundering careers were more by choice and personal inadequacy. Work was seen as an adventure, a place to prove one’s self and worth.

a. By contrast, and particularly in this post-“Great Recession” environment, Gen X and Millennials face fewer opportunities and greater challenges to launch their careers of choice, let alone excel in them. Perhaps more than any other since the Depression, many may be found in lower level “bridge” jobs, if not completely unemployed. Combine this with their cultural bias toward balanced lives, work may be more often seen as a contract and means to an end. As such, it can be demoted to lower priority compared with their personal enjoyment and fulfillment. They may be more readily perceived as “slackers” and feeling entitled to more than may be deserved.

2. Financial Self Sufficiency: Boomers grew up facing clear expectations that they become self-sufficient upon finishing school. Self-sufficiency meant that they could start and support their own separate household with little or no assistance from their parents.

a. Many Gen Xers and Millennials by comparison face considerable financial burden from substantial debts such as school loans. Combining this with fewer career opportunities that an uncertain economy brings, and we see many needing parental support and even living at home much longer. This combined with their cultural bias to do things “their own way,” it is easy to see how Boomers may feel critical and perhaps intolerant of their children’s lack of financial success.

3. Family Success: Although Boomer’s were known to postpone their family launch until later in life, their being able to build a traditional family has been seen as a measure of responsibility and achieving adulthood.

a. Younger generations, by contrast, have more cultural flexibility than ever. While some may choose a traditional family structure, others may consider what best meets their unique needs. Some may be attracted to non-traditional options such as remaining single, co-habitation, etc. Bottom line, an heir’s progress toward their eventual family environment may not be the same gauge of competency that it once was.

4. Life Resiliency: The old adage of “making lemonade out of lemons” has rarely been seen as a more important skill than today with all of its challenges. Boomer optimism and “can do” philosophy-despite-the-hurdles have been legendary traits of this generation. So they may find themselves less sympathetic to discouragement and pessimism that their heirs may express.

a. Gen Xers and Millennials have seen an increase of cynicism, disaffection, and bleakness among their ranks, which is no small wonder considering the challenges we as a society face. The fact is, many of today’s young people see the economy’s anemic recovery as more than just a temporary setback. Rather, the dour environment may very well be costing them the future they once took for granted. The resulting malaise they feel may be met with intolerance by Boomer’s, whose “just hunker down” mentality worked for them so well during their life challenges.

In short, assessing our heir’s competency by these traditional measures may not give us a comprehensive gauge of success. A more objective view may be had by focusing instead on our heir’s actual skill level in several key areas. The expectation is not to develop professional level expertise; rather that heirs demonstrate their willingness to assume responsibility to address these for themselves and their family unit.

1. Budgeting: Managing cash flow and living within one’s means

2. Debt Management: Systemic reduction of education loans, credit cards, mortgages, etc.

3. Savings and Investing: Allocating budget surplus toward future goals

4. Adversity Protection: Assuring loved ones will be financially secure if tragedy strikes (life, disability, liability and medical insurance)

5. Managing Employee Benefits: Optimizing employer programs for protection and savings

6. Estate Planning: Assuring that affairs will be properly handled in case of death or disability

7. Income Tax: Proactively managing affairs to help minimize tax liability

Many heirs have found it helpful to first consider an introspective assessment of their current skill level and areas where they may appreciate further assistance. The attached Financial Scorecard has proven itself a helpful tool in this regard. Where couples are involved, having each complete their own assessment, then comparing their responses can spark candid conversations that can in turn help address varying perceptions. The result may bring the couple closer and ensure everyone is on the same page.

Certainly every generation experiences their own challenges that seem daunting at the time. The eventual success that Gen Xers and Millennials may eventually enjoy will be a function of the encouragement their Boomer parents can offer by creating a supportive, directive, yet non-blaming environment. They likely will have to do more with less compared to those who preceded them which, while difficult, could very well offer a similar character-building opportunity that WWII gave to our “Greatest Generation.” Since many Gen Xers and Millennials will one day be inheritors of considerable wealth, much can be gained by teaming with their Boomer parents in a constructive manner.

This information is not considered a recommendation to buy or sell any investment or insurance and is being provided for information purposes only and is not a complete description, nor is it a recommendation. We strongly recommend an advanced tax and estate planning expert be contacted for further information since Wells Fargo Advisors Financial Network LLC (WFAFN) does not provide tax or legal advice. Any opinions are those of Mitchell Kauffman and not necessarily those of WFAFN. The information has been obtained from sources considered to be reliable, but Wells Fargo Advisors Financial Network does not guarantee that the foregoing material is accurate or complete. Prior to making a financial decision, please consult with your financial advisor about your individual situation.

Mitchell Kauffman provides wealth management services to corporate executives, business owners, professionals, independent women, and the affluent. He is one of only five financial advisors from across the U.S. named the industry’s most qualified Financial Advisor through Research magazine’s Hall of Fame in 2010.

Inductees into the Advisor Hall of Fame have passed a rigorous screening, served a minimum of 15 years in the industry, acquired substantial assets under management, demonstrate superior client service, and have earned recognition from their peers and the broader community.

Kauffman’s articles have appeared in national publications, and he is often quoted in the media. He is an Instructor of Financial Planning and Investment Management at the University of California at Santa Barbara.

For more information, visit www.kwmwealthadvisory.com or call (866) 467-8981. Investment products and services are offered through Wells Fargo Advisors Financial Network LLC (WFAFN), Member SIPC. KWM Wealth Advisory is a separate entity from WFAFN.

______________________

i Great Wealth Transfer Will Be $30 Trillion‐Yes, That’s Trillion With A T by Cam Marston, CNBC On‐Line July 22, 2014, http://www.cnbc.com/2014/07/22/great-wealth-transfer-will-be-30-trillionyes-thats-trillion-with-a-t.html

ii Preparing Heirs by Roy Williams and Vic Preisser, Robert D. Reed Publishers 2003, Pg. 36

iii The Long and the Short of Baby Boomer Balance Sheets by Benjamin Mandel and Livia Wu, J.P. Morgan Investment Insights Oct. 2015

{kind=link}